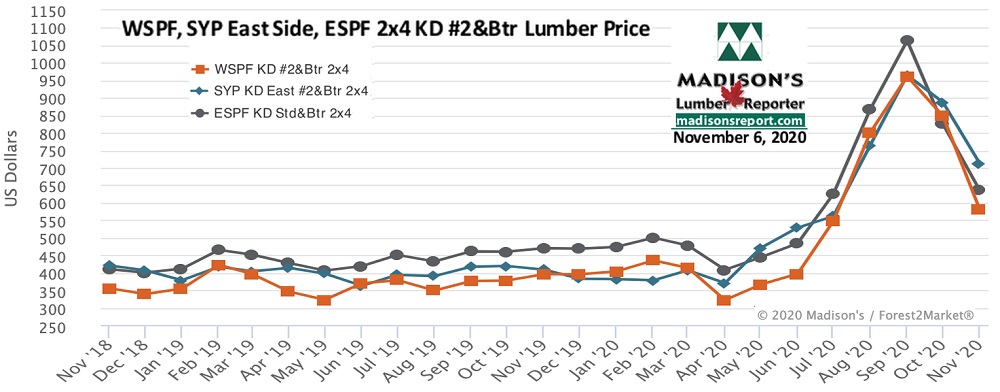

North American construction framing dimension softwood lumber prices did correct down a bit more last week, however demand remained quite strong for the time of year while supply was still quite constrained, according to Madison’s Lumber Reporter.

Customers called around to sawmills and secondary suppliers, at wholesalers and reloads, in search of the wood they needed for ongoing projects. Producers were still spending quite some time locating bits and pieces of wood for customer fill-in needs, but there was also a resurgance of new orders to put on the books. Sawmill order files, which had been an unprecedented (for autumn) five weeks just last month, were down to two weeks or less. That is very strong for the time of year. Usually by November buyers can get prompt wood at any manufacturer. Data for the US housing market — new building, sales, prices, construction employment and spending — are all up drastically compared to historical norms. A strong sales market for softwood lumber is expected to continue right through the Holiday Season and into the beginning of next year.

In the west, sawmills need the winter freeze to arrive sooner rather than later in order to be able to get trucks into the forest and logs into their yards.

Last week, Western S-P-F producers in the United States corrected their asking prices for what they hoped would be the last time this year. Scores of buyers found their trading levels or were otherwise forced off the fence by external factors that made them extra nervous about the depleted state of their inventories. The frequency of counter offers waned significantly as everyone seemed to be scrambling for the same wood pile all at once. Sawmills still had prompt wood available late in the week but were confident they will be building an order file before long. Demand in November kicked off with a bang according to traders.

Western S-P-F sawmills in Canada described sales that came back hard last week after an October they’d sooner forget. Even as prices of #2&Btr dimension tumbled another $40 to $80, to land at what producers hoped would be the bottom, sawmill quoting levels were still historically high. Players noted that a few swirling factors generated last week’s big buy-in; most notably uncertainty surrounding the US Presidential election results, a strong up-limit move in futures, and the November inventory tax cutoff for US customers. One large producer declared Tuesday their biggest day of the year in terms of sales volume.

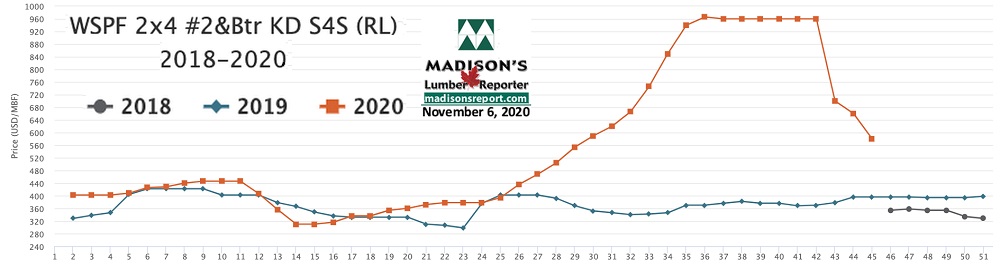

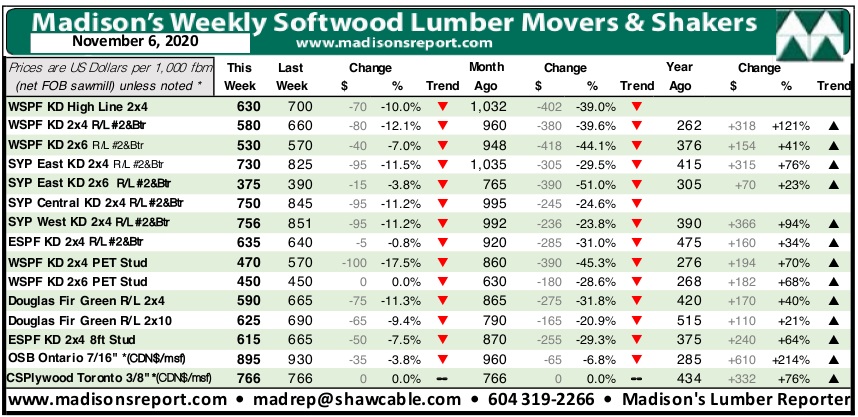

For the week ending November 6, 2020 the price of benchmark softwood lumber commodity item Western S-P-F KD 2×4 #2&Btr continued down but by a lesser degree than the past few weeks, dropping -$80, or -12%, to US$580 mfbm, said Madison’s Lumber Reporter. This week’s price is -$380, or -40%, less than it was one month ago. Compared to one year ago, this price is up +$184, or +46%.

Closing the enormous gap of earlier this year, compared to the 1-year rolling average price of US$530 mfbm, last week Western S-P-F KD 2×4 #2&Btr was selling for +$50, or +9% more, and was up +$132, or +29%, compared to the 2-year rolling average price of US$448 mfbm.

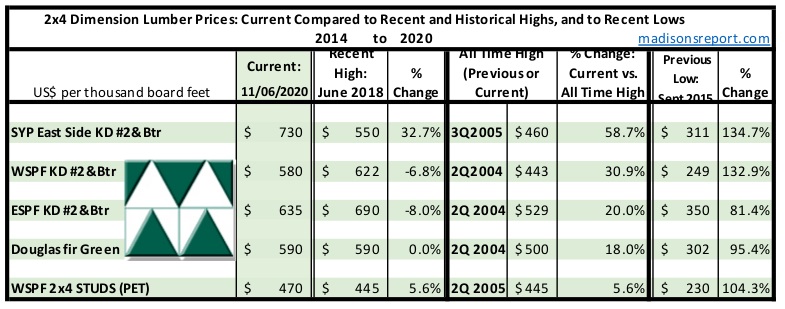

The below table is a comparison of recent highs, in June 2018, and current November 2020 benchmark dimension Softwood Lumber 2×4 prices compared to historical highs of 2004/05 and compared to recent lows of September 2015:

Thank you to Lesprom for their article on North American Softwood Lumber Prices Correct Further

If you would like to see the original article, you can view it here